"*" indicates required fields

Understanding Homeowners Insurance Risks in Raleigh, NC

A Brief Background on Raleigh, NC

Raleigh, the capital city of North Carolina, is located in the central part of the state, forming part of the Research Triangle metropolitan region along with Durham and Chapel Hill. Named after Sir Walter Raleigh, the city was established in 1792 and has grown into a bustling hub of education, technology, and culture. Its strategic location, combined with a mild climate, has made Raleigh an attractive place to live. However, like any city, it has its own set of risks that can impact homeowners, especially concerning home insurance.

Geographical and Historical Context

Geographically, Raleigh is situated in the Piedmont region, characterized by rolling hills and numerous small rivers and streams. This location subjects it to a variety of weather patterns and natural events. Historically, Raleigh has experienced significant growth, transforming from a small, sleepy town into a dynamic urban center. This growth, however, has not been without its challenges, particularly in the realm of natural disasters and weather-related incidents.

Types of Risks Leading to Home Insurance Losses in Raleigh, NC

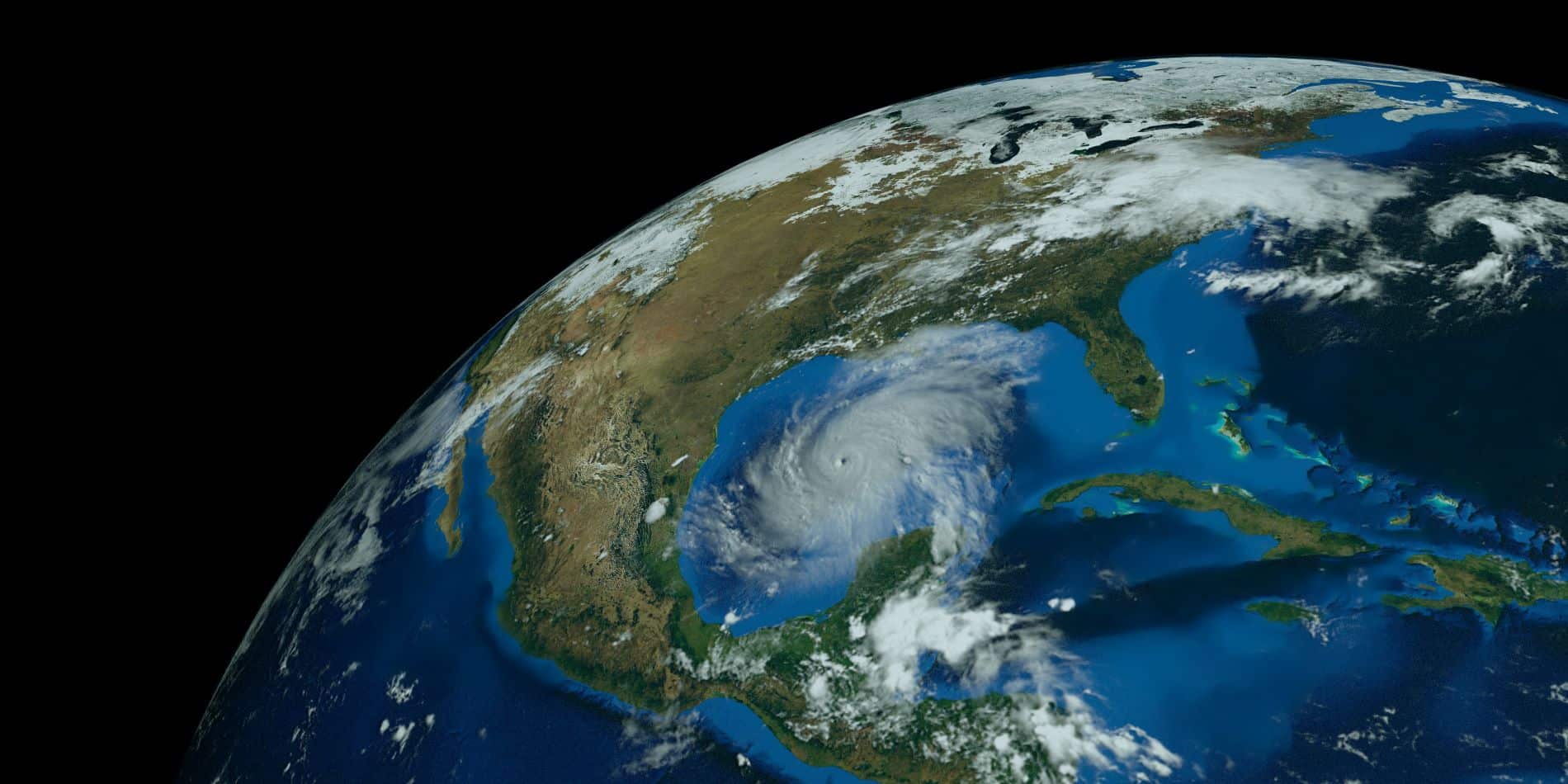

- Severe Weather Events:

- Hurricanes and Tropical Storms: Although Raleigh is inland, it is not immune to the effects of hurricanes and tropical storms. The remnants of these storms can bring heavy rain, strong winds, and flooding.

- Thunderstorms: Frequent in the summer months, these can bring heavy rain, hail, and damaging winds, leading to significant property damage.

- Tornadoes: While not as common as in the Midwest, North Carolina still experiences tornadoes, and Raleigh has seen its share of these destructive events.

- Flooding:

- Raleigh’s numerous rivers and streams can overflow during heavy rains, leading to flash flooding. Urban development has also increased surface runoff, exacerbating the risk.

- Winter Storms:

- Raleigh occasionally experiences ice storms and heavy snowfalls that can damage roofs, cause trees to fall on properties, and lead to power outages.

- Fire Risks:

- Both wildfires and residential fires pose significant risks. Prolonged dry periods can increase the likelihood of wildfires, while aging electrical systems in older homes can lead to residential fires.

- Burglary and Vandalism:

- Property crime, though lower than the national average, still poses a risk, particularly in certain neighborhoods.

Historical Events Leading to Significant Home Insurance Claims in Raleigh

- Hurricane Fran (1996):

- One of the most devastating hurricanes to impact Raleigh, Fran caused widespread damage with wind speeds of up to 79 mph in the city. Thousands of homes were damaged, and the city faced extensive power outages and flooding. The total damage in North Carolina was estimated at $2.4 billion, with a significant portion attributed to Raleigh.

- Hurricane Floyd (1999):

- Though the hurricane’s center was further east, Raleigh experienced heavy rainfall leading to severe flooding. The Neuse River and other local waterways overflowed, causing substantial water damage to homes and infrastructure. The state’s total damage exceeded $6 billion, with flooding being the primary cause of loss.

- April 2011 Tornado Outbreak:

- A series of tornadoes hit Raleigh and surrounding areas, causing extensive damage. The EF-3 tornado that struck Raleigh damaged over 1,000 homes and led to numerous insurance claims for roof damage, structural damage, and total losses.

- Winter Storm Pax (2014):

- This storm brought heavy snow and ice to Raleigh, causing tree limbs to break and fall onto homes, roofs to collapse under the weight of snow, and widespread power outages. The ice accumulation led to significant property damage and numerous insurance claims.

- Hurricane Florence (2018):

- Though its impact was more severe along the coast, Florence brought heavy rains and flooding to Raleigh, leading to substantial water damage. The storm also caused wind damage and power outages, contributing to a high volume of insurance claims.

Mitigating Homeowners Insurance Risks in Raleigh, NC

Given the variety of risks that can impact homeowners in Raleigh, it is crucial for residents to take proactive steps to mitigate these risks and ensure adequate insurance coverage.

- Flood Insurance:

- Despite not being in a coastal area, Raleigh’s susceptibility to flooding makes flood insurance a wise investment. Standard homeowners insurance does not typically cover flood damage, so an additional flood policy is essential.

- Wind and Hail Coverage:

- Homeowners should review their policies to ensure they have adequate coverage for wind and hail damage, which are common during hurricanes and thunderstorms.

- Roof Maintenance:

- Regular inspection and maintenance of roofs can prevent minor issues from becoming major problems during storms. Reinforcing roofs and installing impact-resistant shingles can also reduce damage.

- Tree Maintenance:

- Keeping trees trimmed and removing dead or weak limbs can prevent them from falling on homes during storms, reducing the risk of significant damage.

- Home Security:

- Installing security systems can deter burglars and reduce the risk of property crime. Many insurance companies offer discounts for homes with security systems.

- Emergency Preparedness:

- Having an emergency plan and supplies can help families respond quickly to severe weather events, minimizing injury and damage. This includes having a disaster kit, a family communication plan, and knowing local evacuation routes.

In Closing

Raleigh, NC, is a vibrant and growing city, but its residents must remain vigilant about the various risks that can impact their homes. From hurricanes and flooding to winter storms and property crime, understanding these risks and taking appropriate measures can help homeowners protect their properties and ensure they have the necessary insurance coverage. By learning from past events and staying prepared, Raleigh residents can mitigate the impact of natural disasters and other hazards, securing their homes and their peace of mind.

FAQ on High-Risk Homeowners Insurance

General High-Risk Homeowners Insurance

Q: What is high-risk homeowners insurance? A: High-risk homeowners insurance is a type of policy designed for homes that are more likely to experience claims due to location, condition, or other factors. These homes may face higher premiums due to the increased likelihood of damage or loss.

Q: What factors contribute to a home being considered high-risk? A: Factors include geographical location (e.g., flood zones, hurricane-prone areas), the age and condition of the home, the presence of certain hazards (e.g., old electrical systems), and the history of insurance claims on the property.

Q: How can I lower my high-risk homeowners insurance premiums? A: Improving home security, maintaining the property (e.g., roof and electrical updates), installing disaster-resistant features, and shopping around for different insurance providers can help lower premiums.

High-Risk Homeowners Insurance in North Carolina

Q: What makes North Carolina a high-risk area for homeowners insurance? A: North Carolina is prone to hurricanes, tropical storms, flooding, and occasional winter storms. These natural events increase the likelihood of property damage, making some areas high-risk.

Q: Are there specific areas in Raleigh, NC, that are considered high-risk? A: Areas near rivers and streams, low-lying areas prone to flooding, and neighborhoods with older homes may be considered higher risk due to their susceptibility to water damage and other issues.

Q: Does homeowners insurance in Raleigh cover hurricane damage? A: Standard homeowners insurance typically covers wind damage from hurricanes but may not cover flood damage. Homeowners may need separate flood insurance to be fully protected.

Q: What should I do if I live in a high-risk area in Raleigh? A: Ensure you have adequate coverage for the specific risks you face, such as flood insurance. Regularly maintain your property, invest in upgrades to make it more disaster-resistant, and stay informed about local weather patterns and risks.

Q: Can I get insurance if my home has been previously damaged by severe weather? A: Yes, but it might be more expensive, and insurers may require that certain repairs or upgrades be completed to reduce future risks. Shopping around for the best policy and working with an insurance agent can help find suitable coverage.

Recent Posts

September 10, 2024

2024- Are Burglary Claims Still a High Risk?

Burglaries are a persistent threat to homeowners across the U.S., with over one million break-ins occurring annually. Even though burglary rates have decreased...

September 7, 2024

2024 Atlantic Hurricane Season Predictions

All Early Predictions Call for a Busy 2024 Atlantic Hurricane Season Forecasters are predicting an exceptionally active Atlantic hurricane season in 2024. The...

August 23, 2024

Top High-Risk Home Insurance Factors

When you own a home, one of the most important things you need is home insurance. This insurance helps protect your house and...